Imagine this: As a dentist or dental associate, you’ve got patients coming in for everything from routine check-ups to more intricate procedures. But instead of patients footing the full bill that you’d usually charge, they’re only shelling out a small, fixed amount. Sounds like a pretty good deal for the patients, right? That’s the essence of Copay insurance plans.

A Copay insurance plan works like this: the policyholder only has to pay a fixed amount for a particular service. This predetermined payment is known as the “copay.” For instance, let’s say a patient strolls in for a routine check-up. With their copay insurance plan, they might only need to cough up $30 at the time of the appointment, no matter what the total cost of the check-up is. The rest of your fee is taken care of by the patient’s insurance company. That $30 your patient pays is what we call the “copay”.

A low copay insurance plan operates on the same principle, but with a lower out-of-pocket cost for the policyholder, the patient. Now, you might think this doesn’t affect you since the insurance company picks up the tab. But it’s not quite that simple in all cases.

Let’s take a deeper look into how a low Copay insurance can affect your dental business.

- The heavy hitters in the low copay insurance world are Delta Dental, Humana, Cigna, Aetna, and United Healthcare. You’re likely to come across these guys pretty often.

- As a dentist, you’re pretty much tied to accepting whatever rate the insurance company has negotiated for a particular service if you have signed up with the insurance carrier. Doesn’t matter if it’s less than what the treatment actually costs you – you’ve got to take it as full payment.

- The patient only needs to cough up a small part of the total cost of treatment, after which insurance is supposed to cover the rest. But collecting this payment from insurance can be a real hassle. In what other industry do you provide a service and then maybe, just maybe, collect payment two months later? It’s a unique situation, to say the least.

- Plus, let’s not forget about the possibility of insurance companies delaying or even denying payments. That leaves your office trying to collect the remaining balance from the patient, which can be a big or small amount. This can put a strain on your office’s financials as you’ve now got to chase down the patient for the remaining payment, likely months after the treatment was completed. It is a difficult conversation to say the least.

Let’s play out a real-world scenario to get a handle on all this.

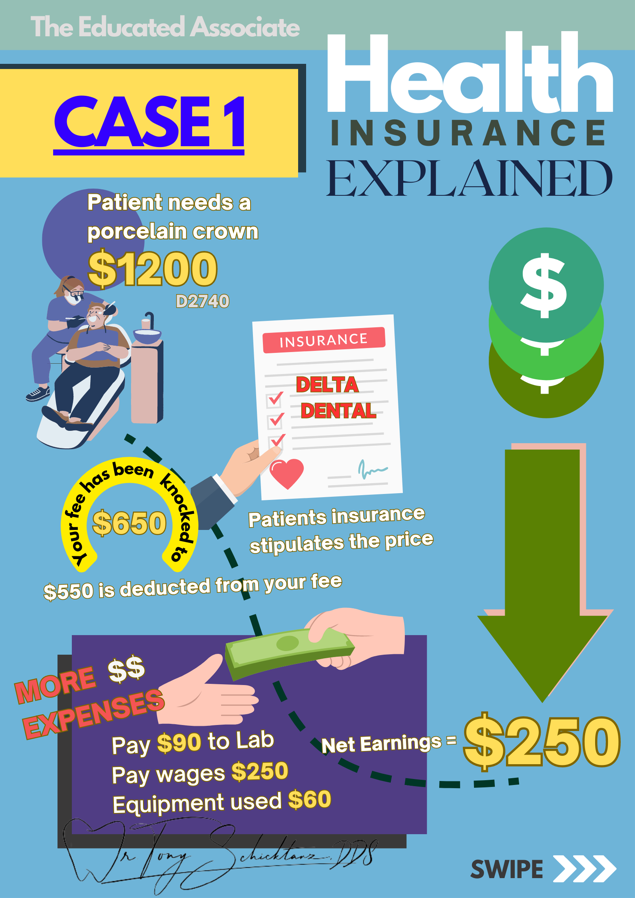

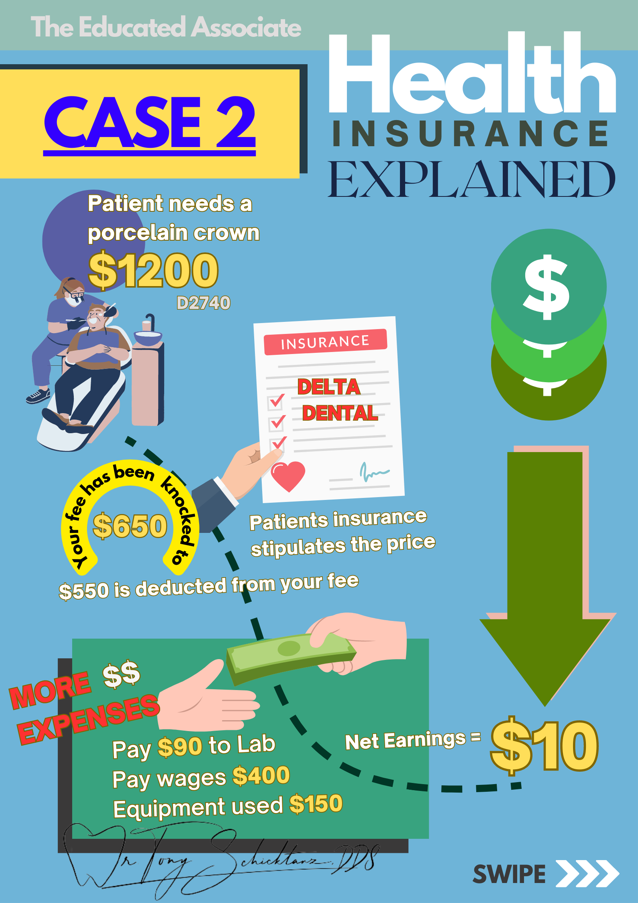

- Imagine a patient needs a porcelain crown (D2740), which usually costs about $1200, UCR fee. But, they’re covered by Delta Dental’s Low Copay insurance. The rate negotiated with Delta Dental for a porcelain crown is $650. That means right off the bat, $550 is just… gone. In this example the patient has a copay of 25%.

- Now, the fee you have to pay to the dental lab for that crown? That’s $90.

- Then, there are the salaries for the office staff and the associate doctor for their time and effort which can be between $250 to $400.

- Don’t forget about the materials – the anesthetic, the burs, the chair time, etc., which can be anywhere from $20 to $150.

- The patient? They pay the 25% of $650 and Delta Dental’s plan is supposed to cover the rest.

So let’s break this down:

- In the first scenario, your Net Earnings (NE) = ($1,200 – $550) = $650 – ($90 + $250 + $60) = $250.

- But in another scenario, the NE could be = ($1,200 – $550) = $650 – ($90 + $400 + $150) = just $10.

So, you do this whole procedure, the patient walks out with a shiny new crown, and you get $650 from Delta Dental and the patient if they each hold up their ends of the deal. After you’ve paid the lab, your staff, and covered the materials, you’re hoping there’s some cash left over to keep the lights on and the business running. But with these contracted rates, it’s getting harder and harder to stay profitable. All it takes is a few extra materials, a bit of extra chair time, or any other unexpected cost, and suddenly, you’re not making any money.

That’s why it’s crucial to think about how these low copay insurance plans affect your dental practice. They might be fantastic for patients, but they can also put a serious dent in your bottom line.

Big thanks to Dr. CL Howe for inspiring this post!

Remember, we’re all in this dental game together, so let’s help each other out!

If you have anything to add or have any questions, please reach to me directly through the “Contact me” button on the website and schedule a free 10-minute phone call. As always, stay drilling my friends.